Criminal organizations are using cutting-edge technologies to devise creative financial illicit activities. Covid-19 also influenced the nature and the scope of money laundering threats. The scale of money laundering is difficult to assess, the UN Office on Drugs and Crime estimates that between 2 and 5% of global GDP is laundered each year. That’s between EUR 715 billion and 1.87 trillion each year.

The complex fight against money laundering and terrorist financing requires new and creative measures for global financial stability and security. The regulatory environment is now catching up by using technological innovation. There is a sense of urgency in the industry and an increased focus on regulatory technology (Regtech) to support anti-money laundering (AML) and compliance.

The European Commission is taking bold measures to fight money laundering. It has published a comprehensive new legislative package to reform its AML regime. This includes the proposal for a new EU Anti-Money Laundering Authority (AMLA) with direct supervisory powers. The AMLA and the 6AMLD, and are massive steps forward to implement stricter controls and tackle evolving criminal methods.

The scale of the work necessary to comply with the 6AMLD cannot be underestimated by obliged entities and their stakeholders. It replaced the 4th and 5th, with new rules relating to supervisory bodies. The directive also extends criminal liability and accountability beyond physical persons, meaning legal entities, such as companies or partnerships, will also become subject to criminal penalties.

.

.

Regulatory expectations and increasing enforcement actions are driving obliged entities to comply with current and emerging regulations. This includes carrying out customer due diligence (CDD) on clients and, in case of suspicions, reporting these suspicions on time.

The focus of AML supervisory programs includes enhancing a risk-based approach to AML. The implementation of the 6AMLD is a great opportunity to use technology and compliance expertise to develop and maintain efficient and innovative risk-based AML solutions that are faster and at a lower cost.

The EU’s proposals will put pressure on the UK and other countries to take corresponding steps to improve ongoing supervision and enforcement, so they are not seen as jurisdictions threatening the EU. All regulated entities from outside the EU will find it challenging to operate in any member state without complying with the 6AMLD. Operations undertaken in the EU will come under the directive and lack of compliance will have a negative impact when looking to gain access to the relevant markets.

.

6AMLD Introduces New Offences Including Cybercrime & Environmental Crime

The 6AMLD clarifies preceding directives by defining offences and penalties to target money laundering in the digital space. The directive also brings a wider definition of money laundering, an extension of criminal liability to any legal persons involved, and severer penalties for money laundering offences. It closes loopholes that criminals have been exploiting for years; it further recognises that to use criminal law to effectively tackle money laundering, it is essential to have rapid and efficient cross-border cooperation.

The 6AMLD will replace the existing directives containing provisions such as rules on national supervisors and financial intelligence units in member states. It includes actions related to “aiding and abetting” and “attempting and inciting” money laundering. This means that criminal liability will be extended to the natural persons (enablers) who act as accessories to the criminal activities. Its implementation will require comprehensive training, risk assessments and updated internal policies and procedures to reflect changes such as:

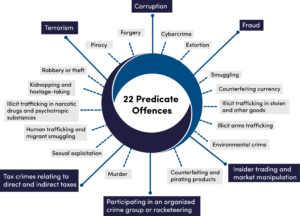

- The uniform list of 22 predicate money laundering offences, and the harmonisation of the criminal nature of money laundering across the EU.

- The need for staff anti-money laundering training on recognising all predicate offences and on an understanding of the comprehensive definition of money laundering.

- How aiding and attempting to commit money laundering will be an offence. There is the imposition of a minimum five-year prison sentence for serious offences.

- The extension of criminal liability to legal persons and the aggravating circumstances that can be applied for convictions relating to serious offences such as corruption and human trafficking.

- Senior management may be personally liable for corporate crimes under new ‘failure to supervise’ offences.

- Penalties for money laundering offences could include prohibition from public welfare benefits, bans from conducting business or forced wind-up of businesses through which the offences were committed.

Companies moving away from human-based processes towards automation and cutting-edge technologies can improve their efficiencies and at the same time reduce the above risks.

.

22 Predicate Offences

.

The Evolution of the AMLDs & What Will Come in The Future

The key goal of the European Commission is to continue to update AMLDs and create a uniformity of rules to have more effective supervision. Recent breaches have been facilitated by a fragmented legislative landscape. Criminals are constantly creating money laundering schemes to exploit cross-border loopholes in the EU’s single market. The 6AMLD and the AMLA are being implemented to mitigate money laundering threats requiring the Member States to assist each other and ensure information is exchanged in an effective and timely manner.

EU AML directives and regulatory requirements will evolve and get stricter. Continuous changes in technology and innovation and its swift use by criminals will raise new challenges to obliged entities and regulators.

Artificial intelligence (AI) and the adoption of blockchain technology will bring new challenges too. New AML directives will take into consideration threats such as deepfakes to impersonate clients and other forms of AI. As the risk environment is becoming more complex, the AML directives will continue to play an important role in the finance sector security framework. Regulators will use new directives to include more layers of security to scrutinize identity fraudsters and enhance due diligence.

The EU Commission’s recent package on digital finance includes the application of AML rules to the crypto sector and the adoption of the Markets in Crypto Assets (MiCA) Regulation. MiCA also expects crypto-asset service providers to comply with FATF and the 6AMLD to ensure that cryptocurrencies are not being used for illicit activities.

Obliged entities and financial service providers have a clear need to improve their AML solutions due to the pressure and requirements from regulators to mitigate risks.

Given how frequently regulations can and do change collaborating with a Regtech provider such as UBO Service may prove essential for obliged entities to enhance risk management quality, reduce costs, and future-proof their compliance processes. Obliged entities and financial institutions will benefit from faster and more precise information on individuals, businesses, and beneficial owners to prevent and detect AML activities.

.

May 30, 2022 Published by The UBO Service.