Just about the entire cryptocurrency ecosystem has gotten washed out in the past week, as news of government crackdowns and other negative headlines have dominated the discussion.

Not every coin has been plunging, however. One of the generally positive things about the decline in cryptocurrency values is that different assets are reacting in different ways to the selloff.

To be sure, the damage is widespread. Bitcoin has fallen 12% in the past week and Ether, the second most valuable cryptocurrency, is down 21%. Excluding stablecoins, whose values hover around $1 because they are pegged to the dollar, the top 12 coins have all fallen. But others have risen over that period.

Barron’s screened for coins within the top 100 cryptos by market cap that have outperformed over the past week, and found several that have held up.

.

Crypto Survivors

Four digital assets have outperformed as the industry crashes

.

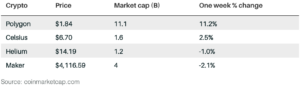

They include coins that aren’t exactly household names, but that are being explored as potentially useful technologies: Polygon, Helium, Celsius, and Maker. It’s dangerous to assume that the relative winners will hold up in the longer-term — cryptocurrencies can move sharply based on trading on opaque unregulated markets and may suffer from low liquidity. With smaller coins in particular, investors need to understand the platform they are buying into because they are essentially investing in an early-stage venture capital start-up.

That said, projects that held up in the selloff are worth watching. One reason some of these coins did well may have been because they dodged some of the overall crypto network’s problems during the selloff.

“One thing we saw during the panic was that both centralized and many decentralized exchanges had issues keeping up with demand,” Matt Hougan, chief investment officer of crypto fund provider Bitwise Asset Management, told Barron’s in an email. “Many centralized exchanges simply went down for periods of time during the selloff, as they were overloaded by traders.”

The Celsius network is known for allowing people to earn interest in their crypto holdings, or to borrow crypto. Celsius says that it has more than 700,000 users and that it is gaining nearly 100,000 users a month. Lending and borrowing are increasingly popular on crypto platforms, and Celsius is becoming a bigger hub for that.

That may have been the case with Polygon, formerly called Matic, the 14th most valuable cryptocurrency. It is a so-called “Layer 2” technology that’s built on top of the Ethereum blockchain, and is meant to make transactions faster and less expensive. Hougan thinks that Polygon was able to bypass some of the congestion in the system during the selloff because it is meant to process more transactions. “Because of this approach, their network wasn’t congested,” he wrote. “As a result, users were able to trade with ease on [Polygon] while other approaches faced challenges.”

Polygon is involved in some of the hottest areas of cryptocurrencies, including working with trading platforms to make it easier to trade non-fungible tokens, or NFTs. Right now, trading NFTs can be expensive because of “gas fees” associated with using trading platforms.

Polygon may have increased for another reason, too — it appears to be better for the environment than some other coins. It uses a “proof of stake” system to validate transactions on the blockchain. Bitcoin uses “proof of work,” a system that’s much more energy intensive. Tesla CEO Elon Musk has criticized Bitcoin’s impact on climate change, causing some proof of stake tokens to outperform proof of work ones.

Helium is a particularly unusual cryptocurrency that is part of a project meant to decentralize wireless communications. Its aim is to get households and businesses to install small telecom hubs on their property — almost like mini cell towers — and then reward them with a token called HNT. The company says it has nearly 42,000 hot spots around the world. It has received funding from New York venture-capital firm Union Square Ventures.

Maker is a token that’s part of another unique finance project within cryptocurrencies. MakerDAO is an organization that created a decentralized stablecoin called DAI that can be lent out without intermediaries. Maker is a key hub in the “defi” movement that is trying to move traditional banking activities to a decentralized network where there are no gatekeepers and people can more easily lend or borrow currencies. The Maker tokens give users a voting stake in the creation of the market, and will presumably rise in value if DAI is used more frequently.

.

By Avi Salzman, May 24, 2021, Published on Barron’s