The Financial Action Task Force addressed DeFi and NFTs in its new proposed draft guidance, but its new definitions might be extremely broad.

The Financial Action Task Force (FATF) has published new draft guidance that, if implemented, could require even decentralized finance (DeFi) platforms to find a way to implement know-your-customer (KYC) rules.

.

The narrative

The Financial Action Task Force (FATF), the inter-governmental watchdog that establishes standards for anti-money laundering (AML) and know-your-customer (KYC) requirements, has published new draft guidance for decentralized platforms.

.

Why it matters

FATF made headlines two years ago when it proposed – and then finalized – guidance urging nations to implement KYC requirements for all crypto exchanges. The so-called Travel Ruledefined virtual asset service providers (VASPs) as businesses that transfer funds in the form of cryptocurrency (i.e., crypto exchanges, among others) and mandated that the businesses should have KYC information for both the sender and the recipient of these transactions.

Countries are beginning to implement these recommendations – South Korea recently brought new anti-money laundering (AML) rules into effect, resulting in at least one major exchange shuttering its operations in the country.

This month’s updated draft guidance massively expands the types of entities that might fall under FATF’s umbrella.

.

Breaking it down

FATF’s new draft guidance, published on March 19, now draws a distinction between fungible tokens and non-fungible tokens (NFTs), adds descriptors for decentralized exchanges and decentralized finance (DeFi) and specifies who might be held liable for enforcing KYC requirements for DeFi platforms, according to my colleague Ian Allison:

“NFTs and DeFi present additional challenges to the FATF, which is already struggling to graft money-laundering rules onto pseudonymous-by-design transactions in the flourishing cryptocurrency industry.”

In other words, FATF moved quickly in response to the rapid growth of NFTs and DeFi over the past year. The updated guidance, if finalized, would ask countries to ensure that even DeFi platforms have some form of KYC rules, even if there’s technically no single party responsible for a live network.

“It’s called ‘updated guidance’ but really it is a sweeping expansion of the way FATF thinks about and defines virtual asset service providers in particular. It really is a move by FATF to react in almost real time to some of the technical advances that are really sweeping crypto right now,” said Ari Redbord, a former U.S. Treasury Department official who’s now head of legal and government affairs at TRM Labs.

The expanded VASP definition would include “individual people and groups of people” in the crypto sector who don’t have a traditional financial sector counterpart, said Blockchain Association Executive Director Kristin Smith, who described the current form of the guidance as “problematic.”

In particular, developers who create some sort of decentralized platform and do not maintain any form of control may still be liable for KYC rules, even if they don’t have a role in the platform post-launch, she said.

“They would still have to be accountable for implementing AML/CFT (countering the financing of terrorism) on something they no longer are a part of necessarily,” Smith said. “What the regulators are trying to do is have a centralized entity that is accountable for an anti-money laundering program that doesn’t sit well on top of decentralized networks.”

Amy Davine Kim, chief policy officer for the Chamber of Digital Commerce, said much of the new guidance applies to regulations that have existed for years, but the explanations in the document lead to some odd interpretations.

Some of the DeFi tools are still evolving, she said.

In her view, “sticking with a principles-based, risk-based approach might serve better for a longer-term solution.”

Still, the fact that FATF published draft guidance so soon after the summer of DeFi and the NFT boom shows that it is paying attention to what’s going on with the digital asset world, Redbord said.

Siân Jones, a senior partner at XReg Consulting, believes crypto may bifurcate into regulated and unregulated factions as this regulatory push continues. While the regulated space will shell out the money to comply with regulations and engage with regulated institutions, others would prefer privacy-focused digital currencies, according to a webinar last week.

“There are a whole host of people who are not necessarily doing bad things, but for whom privacy stands as a fundamental in their lives, they will move … together with money launderers. There’s no way of separating them, and this will move to an ever more anonymous crypto,” Jones said.

This may even be more in line with the original Bitcoin envisioned by Satoshi Nakamoto.

Industry participants have until April 20 to file comments if they wish to provide feedback on the draft guidance. FATF will vote to adopt (or not) the recommendations in its June plenary.

Financial Watchdog Group Updates Guidance Affecting DeFi, NFTs

The Financial Action Task Force (FATF), a global financial watchdog organization, has updated its guidance on crypto assets to be more inclusive of recent market changes, including the NFT boom and growing interest in decentralized finance. Siân Jones of XReg Consulting weighs in on what the updated guidance means for crypto regulation.

.

Europe’s evolving regulatory framework

The European Commission proposed some amendments to its Regulation of Markets in Crypto-Assets (MiCA) last month.

Many of these changes won’t really impact the crypto space one way or another – for example, stablecoins will be regulated as e-money, which has its own regulatory regime in the European Union unrelated to MiCA. However, some of the proposals could force crypto businesses to rethink their strategies.

Cristina Carrascosa, a founder and partner at legal boutique ATH21, told CoinDesk that a proposed ban on interest-bearing crypto assets might be the most significant amendment as far as the crypto sector is concerned.

“This means every single staking token will have to be modified, as interest bearing from crypto asset services providers or token issuers will not be allowed. Some of the liquidity provider pools will also have to re-think their business models, and major ‘decentralized’ insurance providers as well,” she told CoinDesk via email.

Interest-bearing crypto products have taken off recently, she noted, and the European Central Bank (ECB) has said a ban may be “critical.”

Jackson Mueller, director of policy and government relations at Securrency, said the proposed changes “really puts [the ECB] at the center of development of the digital asset space in Europe.”

The amendments also appear to insert the European Securities and Markets Authority (ESMA) into the approval process for digital ledger technology (DLT) market infrastructure.

“The only other thing that particularly caught my attention is that in the amendments to the pilot proposal it also includes a definition of ‘settlement coin’ and this is a whole new proposal,” he said.

.

FinCEN’s proposed rule

The comment period for the Financial Crimes Enforcement Network (FinCEN)’s proposed counterparty rule closed yesterday, with some 7,400 comments, according to a public government portal (up from a little over, uh, 7,000 in January). The U.S. government still has to sort through these comments before it can or will make a decision on how it wants to proceed.

As a reminder: This is the proposed rule that would a) require crypto exchanges to file currency transaction reports (CTRs) for aggregate transactions worth more than $10,000 per day, and b) collect counterparty data for unhosted or private wallets. While the first part would bring crypto reporting rules roughly in line with regulations that banks have to follow for fiat transactions, the second was far more controversial.

I don’t really have any insight on how Treasury Secretary Janet Yellen will fall on this. In written responses to the Senate Finance Committee during her confirmation, she said she intends “to ensure a full and substantive review of the proposals, which will include an assessment of how to ensure proper input from stakeholders.”

It’s also worth noting that Deputy Treasury Secretary Adewale Adeyemo was confirmed to his position last week. He’ll be playing a role in the department’s fintech work from what I hear, and I’m interested to see if he expresses any view on this.

.

Biden’s rule

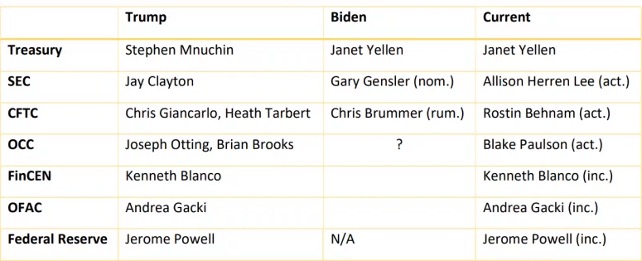

A lot has happened. First off, we’re finally seeing some progress on Gary Gensler’s nomination. To recap: He’s President Joe Biden’s nominee to run the Securities and Exchange Commission, where he’ll oversee like a half-dozen bitcoin exchange-traded fund (ETF) applications and the agency’s ongoing lawsuit against Ripple. On March 10, his nomination was advanced to the Senate out of the Banking Committee. Senate Majority Leader Chuck Schumer filed cloture on his nomination last week, and a vote could happen as soon as the week of April 12 (after the Senate returns from a recess).

The situation with the Office of the Comptroller of the Currency (OCC) is a bit murky at the moment. Last week, American Banker reported that former SEC Commissioner Kara Stein, former Federal Reserve Board Governor Sarah Bloom Raskin and Atlanta Fed President Raphael Bostic are all being considered to run the OCC. Still, University of California law professor Mehrsa Baradaran has support from members of Congress – over 30 Representatives with the Congressional Black Caucus wrote a letter to Biden endorsing her nomination, touting her postal banking and Homestead Act proposals.

Meanwhile, it’s been pointed out to me that Georgetown University law professor Chris Brummer, who was rumored to be Biden’s Commodity Futures Trading Commission pick, has accepted a role on the Board of Directors at Fannie Mae, meaning he may no longer be in the running.

.

Changing of the guard

Key: (nom.) = nominee, (rum.) = rumored, (act.) = acting, (inc.) = incumbent (no replacement anticipated)

.